Table of Contents

- Understanding the Concept of Maxing Out a Credit Card

- How Utilization Affects Credit Scores

- Interest Accrual and Fees

- Short‑Term Financial Consequences

- Reduced Purchasing Power

- Impact on Upcoming Payments

- Long‑Term Credit Score Effects

- Difficulty Securing New Credit

- Insurance and Employment Implications

- Psychological and Behavioral Impacts

- Decision‑Fatigue and Avoidance

- Potential for a Vicious Cycle

- Strategies to Recover and Prevent Future Over‑Extension

- Step‑by‑Step Repayment Plan

- Improving Credit Utilization

- Protecting Against Future Over‑extension

- When to Seek Professional Help

When the balance on a credit card reaches its limit, the immediate impact is more than just a full circle of numbers on a statement. The phrase “maxing out a credit card” signals a turning point that can reverberate through a consumer’s financial life, credit profile, and even daily decision‑making. Understanding this impact is essential for anyone who relies on revolving credit to manage expenses, build credit, or capture rewards.

In the days that follow a maxed‑out card, a series of automatic triggers begin to fire: interest accrues at a higher rate, credit utilization spikes, and the flexibility to cover unexpected costs diminishes. While the short‑term pain is often visible in the next billing cycle, the long‑term consequences can linger for years, shaping the ability to secure loans, rent apartments, or even obtain certain jobs.

This article walks through the cascade of effects that follow a maxed credit card, examines the underlying mechanics, and offers evidence‑based strategies to mitigate damage. By the end, readers will have a clear roadmap for both immediate recovery and sustainable credit health.

Understanding the Concept of Maxing Out a Credit Card

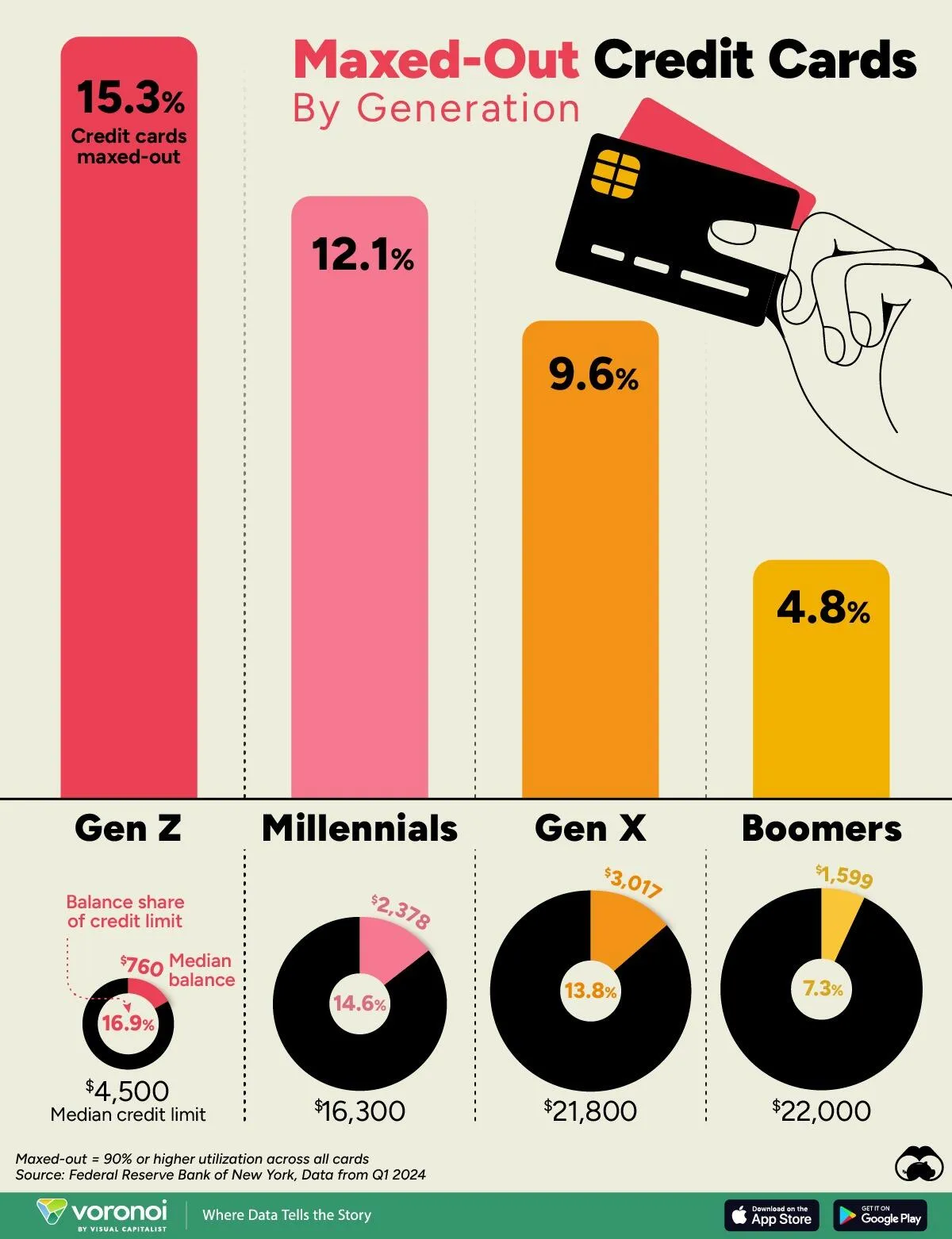

Maxing out a credit card means using enough of the available credit line that the balance approaches or reaches the limit set by the issuer. Most lenders define “maxed out” as a utilization rate of 100 %, but many financial experts recommend staying below 30 % to maintain a healthy credit score. The moment a balance hits the limit, the cardholder loses the ability to make additional purchases without incurring fees or having the transaction declined.

How Utilization Affects Credit Scores

- Credit utilization ratio is calculated by dividing total revolving balances by total credit limits. A sudden jump to 100 % can cause a sharp drop in the FICO score.

- Credit scoring models view high utilization as a sign of increased risk, which can lower the score by 30‑50 points in a single reporting period.

- Even if the balance is paid down quickly, the initial high utilization may remain on the credit report for up to 30 days, affecting new credit applications.

Interest Accrual and Fees

When a card is maxed out, interest compounds on the full balance from the day of the transaction, not just after the grace period. Additionally, many issuers charge a penalty APR that can be significantly higher than the standard rate, and a “over‑limit fee” if the balance exceeds the credit limit, even briefly.

Short‑Term Financial Consequences

The most immediate effect of maxing out a card is the reduction in cash flow. Monthly payments rise because the balance includes both the principal and accumulated interest, often making it difficult to meet other obligations.

Reduced Purchasing Power

- New purchases may be declined, forcing reliance on cash or alternative credit sources that may carry higher costs.

- Emergency expenses become harder to cover, potentially leading to costly short‑term loans or payday advances.

Impact on Upcoming Payments

Because the minimum payment is calculated as a percentage of the balance, a higher balance means a higher minimum payment. Missing a payment can trigger late fees, further increasing the debt burden and damaging the credit score.

Long‑Term Credit Score Effects

Credit scores are built over time, but a single event like maxing out a card can have a lingering effect. Even after the balance is paid down, the historic high utilization remains on the credit report for up to two years, influencing future lending decisions.

Difficulty Securing New Credit

- Lenders reviewing a recent high utilization may view the applicant as a higher risk, resulting in higher interest rates or outright denial.

- Mortgage and auto loan applications often require a credit score above a certain threshold; a dip caused by maxing out can delay major purchases.

Insurance and Employment Implications

Some insurance companies and employers use credit reports as part of underwriting or background checks. A lower score due to maxed‑out credit can lead to higher premiums or reduced job prospects, especially in roles that require financial responsibility.

Psychological and Behavioral Impacts

Beyond the numbers, maxing out a credit card can affect mental health. The stress of mounting debt, fear of collection calls, and the feeling of loss of control can contribute to anxiety and depression.

Decision‑Fatigue and Avoidance

- Cardholders may avoid opening statements, leading to missed payments and further penalties.

- The stress can cause decision‑fatigue, making it harder to stick to a budget or financial plan.

Potential for a Vicious Cycle

When overwhelmed, some individuals turn to additional credit cards or loans to pay off the original balance, creating a cycle of debt that becomes progressively harder to break. Understanding the signs early can prevent escalation.

Strategies to Recover and Prevent Future Over‑Extension

Recovery begins with a clear picture of the debt and a disciplined plan to reduce it. Leveraging tools like a credit card payoff calculator can help estimate the timeline and required payments.

Step‑by‑Step Repayment Plan

- Assess the total debt: Include the principal, accrued interest, and any fees.

- Prioritize high‑interest balances: Allocate extra funds to the card with the highest APR while making minimum payments on others.

- Use a payoff calculator to determine how much extra needs to be paid each month to become debt‑free within a target period. For a deeper dive, see Understanding the Basics of a Credit Card Payoff Calculator.

- Consider a balance transfer to a card with a lower introductory APR, but watch for transfer fees and the end of the promotional period.

- Set up automatic payments to avoid missed due dates and reduce the risk of late fees.

Improving Credit Utilization

- Request a credit limit increase from the issuer; a higher limit lowers the utilization ratio without changing the balance.

- Open a new credit card responsibly, but only if it won’t lead to additional spending temptations. For guidance on managing multiple cards, read How Many Credit Cards Is Too Many? A Deep Dive Into Balancing Benefits and Risks.

- Pay down balances before the statement closing date to ensure a lower reported utilization.

Protecting Against Future Over‑extension

Adopting a proactive mindset can reduce the likelihood of maxing out again. Some practical habits include:

- Budget tracking: Use a budgeting app to monitor spending categories in real time.

- Emergency fund: Build a cash reserve equal to three to six months of expenses to cover unexpected costs without relying on credit.

- Regular credit monitoring: Check credit reports quarterly for errors and to stay aware of utilization trends.

- Freeze the card temporarily during periods of high temptation; learn how to do this safely by reading How to Freeze Your Credit Card Temporarily – The Simple Guide Every Cardholder Needs.

When to Seek Professional Help

If the debt feels unmanageable, consider contacting a certified credit counselor. Non‑profit agencies can negotiate lower interest rates, set up repayment plans, and provide education on credit management.

Recovering from a maxed‑out credit card is a gradual process that blends financial discipline, strategic planning, and psychological resilience. By addressing the immediate financial strain, repairing the credit score, and establishing safeguards against future over‑extension, cardholders can restore stability and regain confidence in their financial decisions.

Ultimately, the impact of maxing out a credit card is multi‑dimensional, affecting numbers on a statement, the health of a credit score, and the wellbeing of the individual. Recognizing each layer equips consumers to act decisively, turn a setback into a learning experience, and build a stronger financial foundation for the years ahead.